Snap Inc., the parent company of the popular social media application Snapchat, has released its financial results for the first quarter of 2026, presenting a complex picture of growth in daily active users (DAU) that is significantly skewed towards emerging markets, while its most profitable regions, North America and Europe, continue to experience user declines. Despite these demographic shifts, the company’s advertising business has demonstrated resilience, showing a steady increase in revenue, albeit overshadowed by persistent high operating costs and an increasingly challenging regulatory and competitive landscape. The report underscores a pivotal period for Snap, as articulated by CEO Evan Spiegel, who has termed it a "crucible moment" for the company’s long-term trajectory.

User Dynamics: A Tale of Two Geographies

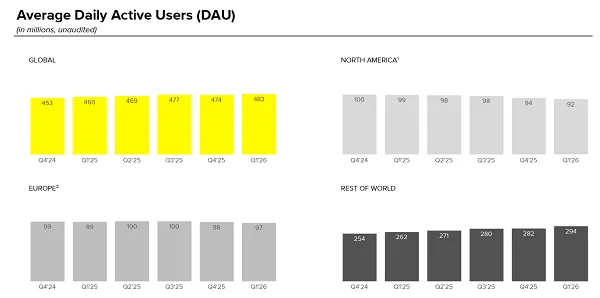

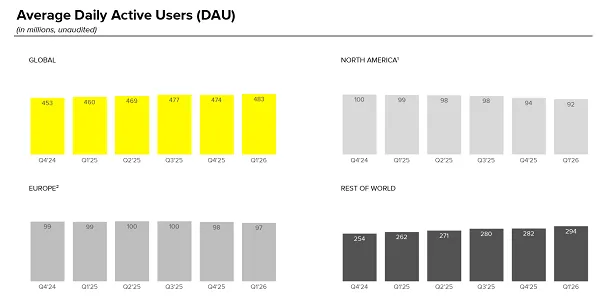

For Q1 2026, Snapchat reported a global Daily Active User (DAU) count of 483 million, an increase of 9 million users from the previous quarter’s 474 million. This surge represents a welcome rebound, particularly considering the 3 million user decline observed in Q4 2025. On the surface, this topline growth might suggest a healthy expansion of Snapchat’s global footprint. However, a deeper dive into the geographic distribution of this growth reveals a critical underlying challenge for Snap’s monetization strategy.

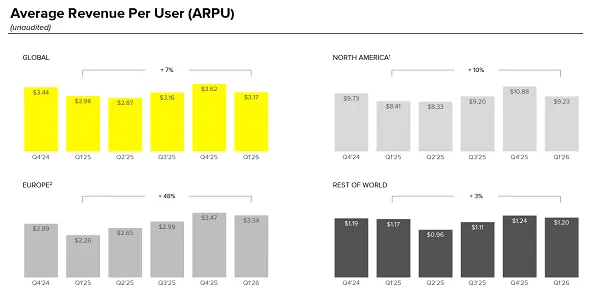

The robust user acquisition is almost exclusively concentrated in regions where Snap is still in the nascent stages of developing its business tools and, consequently, generates significantly less revenue per user. In stark contrast, Snapchat’s two most lucrative markets, North America and Europe, experienced a continued contraction in their user bases. North America, which remains the primary engine for Snap’s revenue, saw its daily usage decline by another 2 million users, settling at 92 million DAU. Similarly, the European market registered a reduction of 1 million users compared to the preceding quarter. This divergence highlights a fundamental disconnect: while Snapchat is expanding its reach, it is simultaneously losing ground in the very markets that underpin its financial viability. The average revenue per user (ARPU) disparity between these regions is substantial, meaning that a user gained in a developing market contributes a fraction of the revenue compared to a user in North America or Europe.

Furthermore, Monthly Active Users (MAU) also saw an increase, reaching 956 million globally, up from 946 million in Q4 2025. While MAU offers a broader view of engagement, the DAU figures are often more closely watched by investors as a key indicator of consistent user habit and platform stickiness. The consistent growth in MAU and overall DAU signals continued relevance on a global scale, but the geographical breakdown remains a significant concern for the company’s bottom line.

Revenue Performance: Ad Business Holds Steady

Despite the mixed user growth narrative, Snap’s advertising business demonstrated a commendable performance in Q1 2026. The company reported total revenue of $1.53 billion for the quarter, marking a respectable 12% increase year-over-year. This growth indicates that Snap’s efforts to diversify its ad offerings and improve ad performance are yielding positive results, even amidst a highly competitive digital advertising environment dominated by tech giants like Meta and Google, and the rapidly ascending TikTok.

Key drivers of this revenue growth included strong performance gains from Sponsored Snaps, an immersive ad format deeply integrated into the Snapchat experience. Moreover, Dynamic Product Ads (DPAs) proved to be a significant success story, with revenue from this segment growing by more than 30% year-over-year. DPAs, which automatically create personalized ads for users based on their browsing history and interests, saw particular growth among small and medium-sized business (SMB) customers. The expansion of the SMB customer base is a crucial strategic win for Snap, as this segment often represents a vast and relatively untapped pool of advertising spend. By appealing to a broader range of brands and advertisers, Snap is attempting to de-risk its revenue streams and build a more resilient ad business.

However, the challenge remains to translate the growing user base in developing markets into commensurate revenue. While the ad business is improving on the monetization front, the chart presented in the original report clearly illustrates the stark difference in revenue generated per user across different regions. This disparity means that for Snap to truly leverage its global user growth, it must significantly enhance its monetization capabilities and ad infrastructure in these developing markets, a task that requires substantial investment and strategic execution.

Operational Efficiency and Cost Management

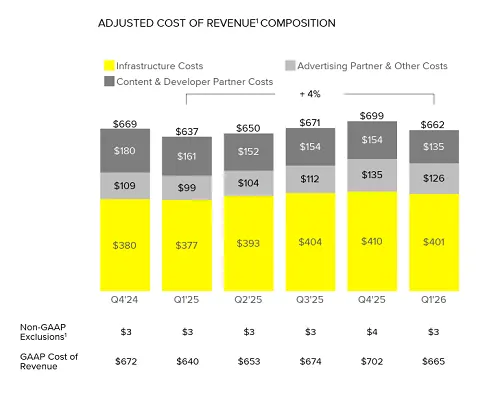

Maintaining a delicate balance between growth investments and operational efficiency continues to be a critical focus for Snap. The company’s costs remain high, a recurring theme in its financial reports. In response to this, Snap has been actively implementing cost-cutting measures, including a significant workforce reduction. Earlier reports indicated that Snap laid off 16% of its full-time staff, affecting approximately 500 employees, as part of a broader effort to streamline operations and improve overall viability. These measures are designed to enhance the company’s financial performance and provide more flexibility as it continues to develop its advertising business and explore new opportunities.

The high cost structure of a global technology company like Snap is often attributed to substantial investments in research and development (R&D) for new features and products, cloud infrastructure to support its vast user base and data processing, and marketing to attract and retain users and advertisers. While necessary for innovation and scale, these expenses exert pressure on profitability, making efficient cost management paramount, especially in a period of mixed user growth and intense market competition.

Regulatory Headwinds: The Age Restriction Imperative

A significant and growing challenge for Snap, and indeed for the entire social media industry, is the increasing global push for stricter age restrictions on social media usage. This movement, largely driven by concerns over the mental health and well-being of young people, as well as issues of data privacy and exposure to inappropriate content, is gaining considerable momentum. Many regions are actively considering or in the process of implementing bans for users under the age of 16, following the precedent set by countries like Australia.

Snapchat is particularly vulnerable to such regulations due to its undeniable popularity among younger audiences, a demographic that forms a substantial portion of its core user base and engagement engine. The tangible impact of these bans was already evident in February when Snapchat reported that Australia’s teen ban had compelled it to lock or disable approximately 415,000 user accounts within that nation. Given Australia’s population of around 27 million, this figure represents a significant percentage of its youth demographic.

The potential for expanded impact across larger European economies is a pressing concern for Snap. Countries like Germany (population ~84 million), the U.K. (population ~69 million), and Spain (population ~49 million) are all actively considering or have introduced legislation for similar teen social media bans. Should these initiatives come to fruition, the cumulative effect on Snap’s user base in key profitable markets could be devastating, further exacerbating the existing user decline trends in these regions. The loss of hundreds of thousands, potentially millions, of young users would not only shrink Snap’s audience but also diminish its attractiveness to advertisers targeting this demographic. This regulatory pressure adds another layer of complexity to Snap’s broader growth plans and represents a significant risk factor for the company’s future.

Strategic Outlook and Future Innovation

CEO Evan Spiegel’s characterization of this period as a "crucible moment" underscores the critical juncture at which Snap finds itself. The company is simultaneously battling established tech giants like Meta (Instagram, Facebook) and Google (YouTube), while also fending off agile startups like TikTok, which has successfully captured a massive share of the youth demographic with its short-form video format. Snap’s ability to navigate these competitive pressures and differentiate its offerings will determine its long-term success.

Snapchat’s investor update last month outlined a multi-pronged growth strategy, focusing on several key pillars:

- Reaching 1 Billion Daily Active Users: While global DAU is growing, the critical issue remains the declining user base in high-ARPU markets. Achieving 1 billion DAU will require not only sustained growth in emerging markets but also a reversal of trends in North America and Europe, or a significant increase in monetization capabilities in new regions.

- Driving Innovation: The article notes that Snap’s innovation has not evolved significantly in recent years, beyond features like Spotlight, which was widely seen as a response to TikTok’s success. While Snapchat continues to pioneer augmented reality (AR) features and Lenses, the lack of truly groundbreaking new platform experiences could hinder its ability to attract and retain users in a crowded market.

- Growing Subscription Revenue: Snapchat+ income is growing, but it remains a minor component compared to its advertising revenue. While subscriptions offer a recurring revenue stream and enhance user loyalty, they are unlikely to fundamentally shift Snap’s financial reliance on advertising in the near future.

- Improving Ad Performance: Snap’s current ad revenue growth is positive, driven by diversification and appeal to SMBs. However, the company’s strategy to find new ad opportunities, such as placing ads in user DMs and expanding placements, carries inherent risks. An influx of ads could lead to user fatigue and complaints, potentially eroding the "connective experience" that defines Snapchat and driving users to less ad-saturated platforms. This delicate balance between monetization and user experience is a constant challenge for social media platforms.

- Launching AR Glasses: Snap is still planning to launch its latest iteration of AR glasses, Spectacles, this year. However, the market for consumer AR wearables remains nascent and highly competitive. Concerns exist regarding the device’s form factor ("chunky, heavy") and its potential inferiority to upcoming offerings from competitors. Meta, for instance, has already released its Ray-Ban Meta smart glasses and has ambitious plans for more advanced AR glasses, codenamed "Project Aria," slated for 2027. Snap’s previous attempts with Spectacles have seen limited commercial success, and the path to widespread consumer adoption for AR wearables is fraught with challenges, including high costs, limited use cases, and design constraints. For Spectacles to be a significant growth driver, Snap would need to demonstrate a compelling value proposition that resonates with a broad consumer base, a feat no company has yet fully achieved in the consumer AR space.

Broader Market Implications and Future Outlook

Snap Inc.’s Q1 2026 earnings report paints a picture of a company facing significant structural challenges despite showing signs of resilience in its core advertising business. The fundamental issue lies in the quality versus quantity of its user growth. While expanding its global footprint is important, the continued decline in its most profitable markets raises questions about its long-term ARPU and overall market capitalization potential.

Analyst reactions to the report are likely to be mixed, acknowledging the steady ad revenue growth but expressing concerns over the persistent user declines in key regions and the mounting regulatory pressures. Investor sentiment will be closely tied to Snap’s ability to demonstrate a viable path to monetizing its growing user base in developing markets and mitigating the impact of age restrictions in its established profitable territories.

The company’s future hinges on its capacity to innovate beyond incremental feature additions, to effectively manage its high cost base, and to navigate the increasingly complex regulatory environment. Evan Spiegel is correct; this is indeed a crucible moment. The coming quarters will be critical in determining whether Snap can successfully transform its user growth into sustainable, profitable expansion, or if it will continue to grapple with the inherent limitations of its current market position and strategic execution. The race to capture the next generation of social media users, coupled with the quest for viable AR hardware, will define Snap’s competitive standing in the years to come.

{kind=link}