The Hidden Reality of Marketing Returns Why Standard ROI Metrics Fail to Measure Real Business Value

In the current landscape of digital commerce, a growing disconnect has emerged between the performance reports generated by marketing agencies and the actual financial health of the corporations they serve. While marketing departments frequently report robust success through metrics like Return on Investment (ROI) or Return on Ad Spend (ROAS), chief financial officers (CFOs) and executive boards are increasingly skeptical. This skepticism is rooted in a phenomenon often referred to as the "Giant in the closet"—a collection of hidden costs and over-attributed revenues that, when fully accounted for, can transform a reported four-fold return into a significant net loss.

The core of the issue lies in the methodology used to calculate performance. For years, the industry standard has relied on a simplified ROI formula that compares traceable revenue directly to media spend. However, as economic pressures mount and the need for fiscal transparency increases, analysts are advocating for a more rigorous, four-tiered approach to measuring marketing effectiveness. This transition from "surface-level ROI" to "Incremental Net Profit ROI" represents a fundamental shift in how businesses evaluate the success of their advertising investments.

The Evolution of ROI Measurement: A Four-Tiered Framework

To understand why marketing budgets are often the first to be reduced during economic downturns, one must examine the levels of financial reporting that exist within most modern enterprises. The discrepancy between what an agency reports and what a business actually earns is typically found in the transition between these four tiers.

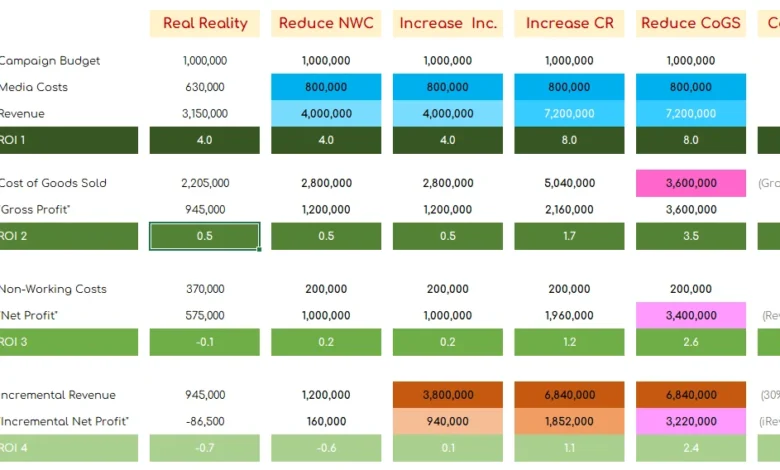

Tier 1: The Agency Standard (ROI 1)

The most common computation used in quarterly business reviews (QBRs) is a simple ratio: (Revenue – Media Costs) divided by Media Costs. In this scenario, if an agency spends $600,000 on digital ads and generates $3.2 million in traceable revenue, they report an ROI of 4.3 (often rounded to 4). From the agency’s perspective, every dollar spent returned four dollars in sales. While mathematically accurate within its narrow scope, this figure fails to account for the fundamental costs of doing business.

Tier 2: Gross Profit ROI (ROI 2)

The second tier introduces the Cost of Goods Sold (COGS). For a business to sell a product—whether it is eyewear, electronics, or automotive parts—it must first manufacture, store, and ship that product. If a product has a 70% COGS (or a 30% gross margin), the $3.2 million in revenue actually only represents $960,000 in gross profit before any marketing costs are deducted. When the $600,000 media spend is subtracted from this gross profit, the remaining $360,000 results in an ROI of 0.6. The "4x return" has already evaporated before accounting for operational overhead.

Tier 3: Net Profit ROI (ROI 3)

The third tier incorporates "non-working media costs." These are the expenses required to make the advertising happen, including agency fees, creative production, ad-tech subscriptions, and internal staff salaries. In many high-performing organizations, non-working costs can represent 40% or more of the total marketing budget. If the total campaign budget was $1 million ($600,000 in media and $400,000 in non-working costs), the net profit after COGS and total spend actually becomes negative. In the case study analyzed, this resulted in an ROI of -0.1, indicating that the campaign lost money even before considering market dynamics.

Tier 4: Incremental Net Profit ROI (ROI 4)

The final and most rigorous tier is "Incrementality." This metric asks the most difficult question in marketing: How many of these sales would have happened anyway? Factors such as brand recognition, seasonal demand, organic search rankings, and existing customer loyalty contribute to sales regardless of specific ad campaigns. If a campaign has an incrementality rate of 30%, it means that 70% of the reported sales were "organic" and merely captured by the ad, not created by it. Accounting for this final factor often reveals an "Incremental ROI" (iROI) as low as -0.7, meaning the company effectively paid to lose 70 cents for every dollar invested.

Case Study: The Anatomy of a $3.2 Million Campaign

To illustrate the impact of these hidden costs, consider a recent campaign for a mid-sized consumer electronics brand. The agency reported a successful quarter with the following data:

- Reported Revenue: $3,200,000

- Media Spend: $600,000

- Reported ROI: 4.33

Upon internal audit by the finance team, the "Real ROI" was calculated by integrating the company’s operational data. The product margin was identified at 30% (COGS of 70%). Furthermore, the internal marketing budget revealed $400,000 in production and agency fees that were not included in the agency’s performance report.

The chronological analysis of the data showed that while the ads were driving clicks, the majority of the customers were returning users who likely would have purchased via direct navigation or organic search. Using a causal inference model, the team determined the incrementality of the campaign was 30%.

The final calculation for ROI 4 (Incremental Net Profit ROI) looked like this:

- Incremental Revenue: $960,000 (30% of $3.2M)

- Incremental Gross Profit: $288,000 (30% margin on incremental revenue)

- Total Campaign Cost: $1,000,000 (Media + Non-working costs)

- Net Incremental Profit: -$712,000

This analysis explains why the CFO viewed the campaign as a failure despite the agency’s claim of a 4x return. The company had essentially subsidized sales that were already going to happen, while failing to cover the production and manufacturing costs of the incremental sales they did generate.

Strategic Implications for Modern Marketing Teams

The realization that traditional ROI metrics may be misleading has prompted a shift in strategy among leading CMOs. To move toward a positive ROI 4, experts suggest a multi-departmental approach that goes beyond simply adjusting ad bids.

1. Optimization of Non-Working Costs:

Marketing teams are being tasked with identifying "excessive" non-working media costs. This includes auditing agency retainers, consolidating bloated marketing technology stacks, and streamlining creative production through AI and automation. Reducing the $400,000 overhead in the previous example is the fastest way to move the needle toward profitability.

2. Focus on High-Incrementality Tactics:

Agencies are increasingly being incentivized based on incremental lift rather than total attributed revenue. This shifts focus away from "branded search" (which often has low incrementality) toward prospecting and acquisition tactics that reach new audiences who were not previously aware of the brand.

3. Integration with Commerce and Engineering:

The responsibility for ROI is shifting from a purely marketing concern to a cross-functional one. If a campaign is driving traffic but the website’s conversion rate is low, the engineering and commerce teams must be held accountable. Similarly, if COGS is too high for a product to ever be profitably advertised, the product engineering team must look for manufacturing innovations to improve margins.

The Role of Brand Marketing and Long-Term Horizon

A common critique of the ROI 4 model is that it favors short-term performance marketing over long-term brand building. However, proponents of the model argue that brand marketing must also be held to a standard of profitability, albeit on a different timeline.

For brand-focused campaigns, the impact horizon typically stretches beyond six months. In these cases, short-term success is measured through "Lift" metrics—calculating the cost per individual lifted in brand awareness or intent compared to a baseline. Long-term profitability is then modeled using advanced attribution, machine learning-based mix models (MMM), and CausalAI to determine how today’s brand spend influences tomorrow’s incremental net profit.

Conclusion: Bridging the Gap Between Marketing and Finance

The tension between marketing departments and finance offices is unlikely to dissipate until a unified standard of measurement is adopted. As long as marketing reports rely on ROI 1 (Media ROI) while the board of directors looks at ROI 3 (Net Profit ROI), budgets will continue to be viewed as discretionary expenses rather than capital investments.

The move toward ROI 4—Incremental Net Profit ROI—is not merely an accounting exercise; it is a survival strategy for the modern marketer. By acknowledging the "Giant" of hidden costs and the reality of organic demand, marketing teams can align themselves with the broader business goals of the organization.

In an era where every dollar is scrutinized, the ability to prove that a marketing campaign delivered actual incremental profit to the bottom line is the only way to ensure that marketing remains a protected and valued component of the corporate budget. As industry leaders often note, ROI 3 is the minimum standard required to survive a CFO audit, but ROI 4 is the gold standard that ensures marketing is the last budget to be cut during a crisis.

{kind=link}